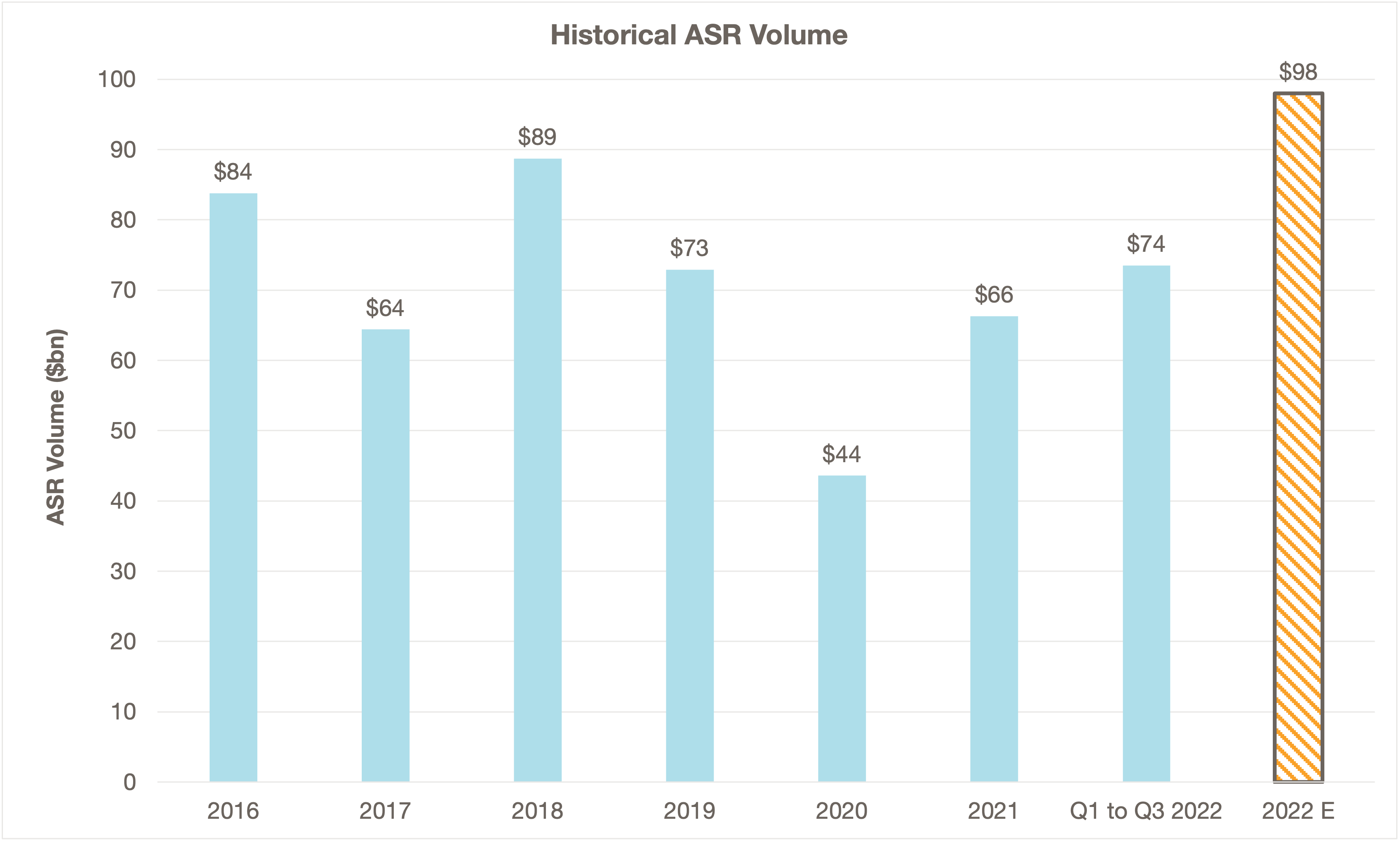

2022 has been a banner year for ASRs with greater volume through the first three quarters than the corresponding period in any year in recent history. There have been 77 ASRs for a total of $73.5bn during this period. ASR terms for companies have never been better given high volatility and rising interest rates. In our latest blog post, we briefly examine what is an ASR, why companies use them, the drawbacks, the current market environment, and why there has been a significant uptick in usage.

Summary Market Statistics

- $73.5bn of ASRs have been executed in in the first three quarters of 2022, which extrapolates to $98bn for the full year

- Volume from Q1 to Q3 2022 was ~40% higher than the comparable period average since 2015

- ASRs represented the greatest share of the buyback market in the last 4 years

- ASR discounts are at historic highs given high market volatility and rising interest rates; some companies are seeing discounts that are 50% better than the average discount since 2015

- Matthews South has advised on over $20bn of ASRs in 2022, which is over a quarter of the market

Source: InsiderScore

What is an ASR?

An ASR is a program in which a company commits to buy an amount of stock from a counterparty (bank) and receives a majority of the shares upfront. Over the course of an ASR, the counterparty purchases stock in the market and the company ultimately buys at the average of the daily prices, less a guaranteed discount.

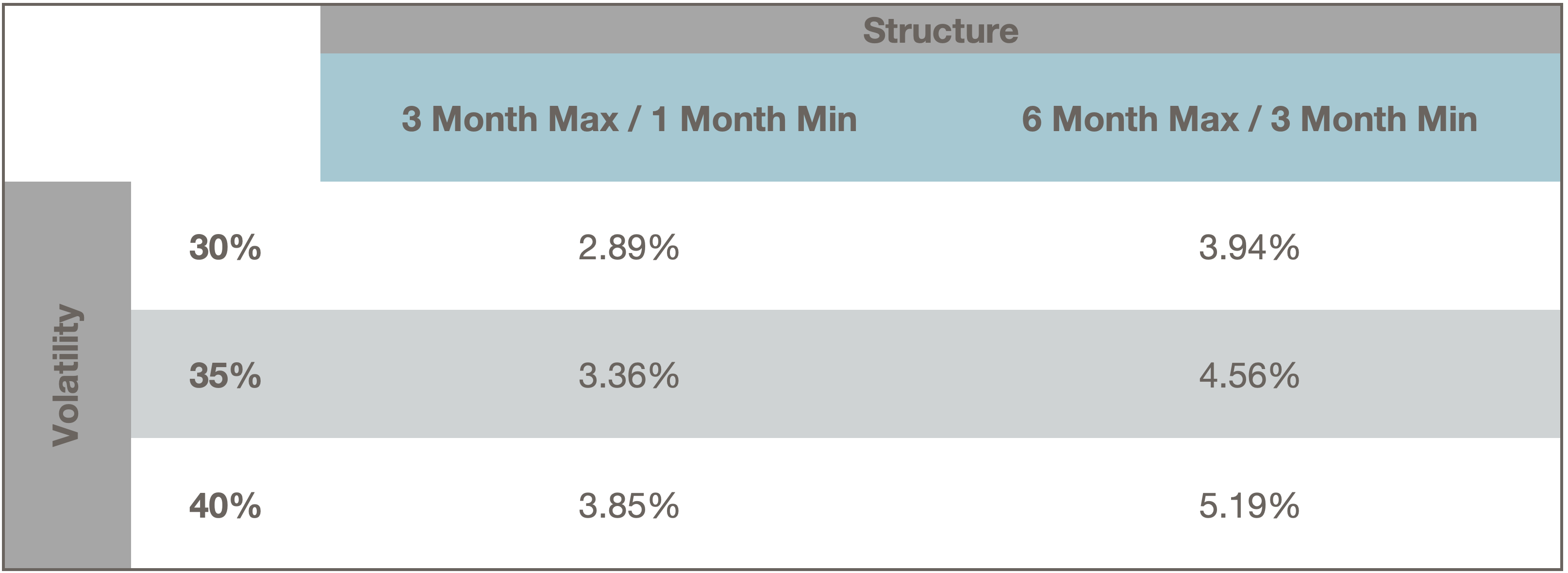

Over 95% of ASRs are structured with a variable maturity option. This gives the counterparty discretion over the time that the ASR is completed (i.e., the period over which the average is calculated). The variable maturity option has value, which is why the company receives an even more meaningful discount to the average price. The value of this feature, and therefore the magnitude of discount, increases with volatility.

Below are example mid-market discounts for two ASR structures at various volatilities:

Assumes 4.63% and 5.08% interest rates for 3 months and 6 months, respectively

Why do Companies Use ASRs?

The high, guaranteed discount to VWAP in an ASR is valuable. While open market plans also deliver discounts, these discounts are uncertain and often much smaller than what is offered in an ASR.

The upfront retirement of shares in an ASR results in a greater impact to the weighted average shares outstanding than an equivalent open market repurchase.

The ASR also has signaling benefits. As a committed program, investors know the company will complete the buyback. It is also an event that lends itself well to a press release, while open market repurchases are made over time and disclosed with earnings.

What are the Drawbacks of an ASR?

ASRs cannot be canceled easily. So, they are only advisable when a company is committed to executing the repurchase in all scenarios.

ASRs are also not advisable for valuation sensitive companies. This is because it is difficult to incorporate price or dollar spend limits in the program.

Additionally, ASRs typically complete early when the stock price trends lower. In these scenarios, the company may be better off foregoing the discount, staying in the market and buying at prevailing, lower stock prices. It is important to recognize that most open market repurchase programs have a similar dynamic, as most companies spend at a greater pace if the stock declines.

Why are ASRs so Popular Now?

2022 may see the greatest amount of ASR volume in recent years. In the first 3 quarters, there were 77 disclosed ASRs totaling over $73bn. Some of the large ASRs this year include:

- S&P Global: $7bn (MS advised)

- Amgen: $6bn

- Bristol-Myers Squibb: $5bn

- Cigna: $3.5bn

- KLA: $3bn (MS advised)

- S&P Global: $2.5bn (MS advised)

While more attractive equity market valuations drive repurchase decisions generally, the current attractive ASR pricing likely explains the increased proportion of repurchases being executed via ASRs.

Volatility is the main driver of variable maturity option value. Greater volatility means larger stock price moves, which allow the counterparty (i.e., bank) to profit more in its hedging activity (buy more when stock is low, and buy less or sell when stock is high). Realized volatility and the VIX index are at historically high levels. As greater volatility increases the option value, the counterparty is more willing to guarantee a higher discount.

| VIX | % of Current VIX | |

|---|---|---|

|

Nov 2022 |

23.7 |

|

|

Nov 2021 |

16.5 |

69% |

|

Nov 2020 |

22.5 |

95% |

|

Nov 2019 |

13.1 |

55% |

|

Nov 2018 |

20.0 |

84% |

Higher interest rates also result in a bigger discount. The counterparty earns interest on the cash paid upfront as it gradually uses the cash to buy shares in the market over the course of the ASR. With greater interest earned, the counterparty is more willing to guarantee a higher discount. The higher discount benefit is generally viewed as not being taxable as income, whereas interest earned on balance sheet cash during an open market program is taxed.

| 6 Month Interest Rate | |

|---|---|

|

Nov 2022 |

5.08% |

|

Nov 2021 |

0.23% |

|

Nov 2020 |

0.25% |

|

Nov 2019 |

1.93% |

|

Nov 2018 |

2.86% |

These two factors translate to pricing that has never been better. To illustrate this, we calculate mid-market ASR discounts for a mega cap technology company since 2015. The discount in 2022 is by far the highest at 4.40% – a full 79 bps higher than the next closest year (2020).

| Date | Mid-Market Discount |

|---|---|

|

15-Nov-22 |

4.40% |

|

15-Nov-21 |

2.75% |

|

15-Nov-20 |

3.61% |

|

15-Nov-19 |

2.74% |

|

15-Nov-18 |

3.49% |

|

15-Nov-17 |

2.72% |

|

15-Nov-16 |

2.53% |

|

15-Nov-15 |

2.93% |

Conclusion

2022 has been a banner year for ASRs by all metrics. Current equity prices are attractive to many companies. Historically high volatility and rising interest rates are contributing to discounts that have never been seen. Given the trend has been better pricing throughout the year, 2023 may be an even bigger year for ASRs.

With higher discounts, there is more room for value to be left on the table. It is important to have an advisor on your side to ensure you receive the best pricing in addition to making the best decisions on structure and documentation.

Personal Views: The views expressed in this report reflect our personal views. This blog post is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. The large majority of reports by us are published at irregular intervals as appropriate in our judgment and ability to produce, so updates may not be made or available even when circumstances may have changed.

No Offer: This analysis is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. You must make an independent decision regarding investments or strategies mentioned on this website. Before acting on information on this website, you should consider whether it is suitable for your particular circumstances. You should not construe any of the material contained herein as business, financial, investment, hedging, trading, legal, regulatory, tax, or accounting advice. The price and value of investments referred to in this analysis and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.