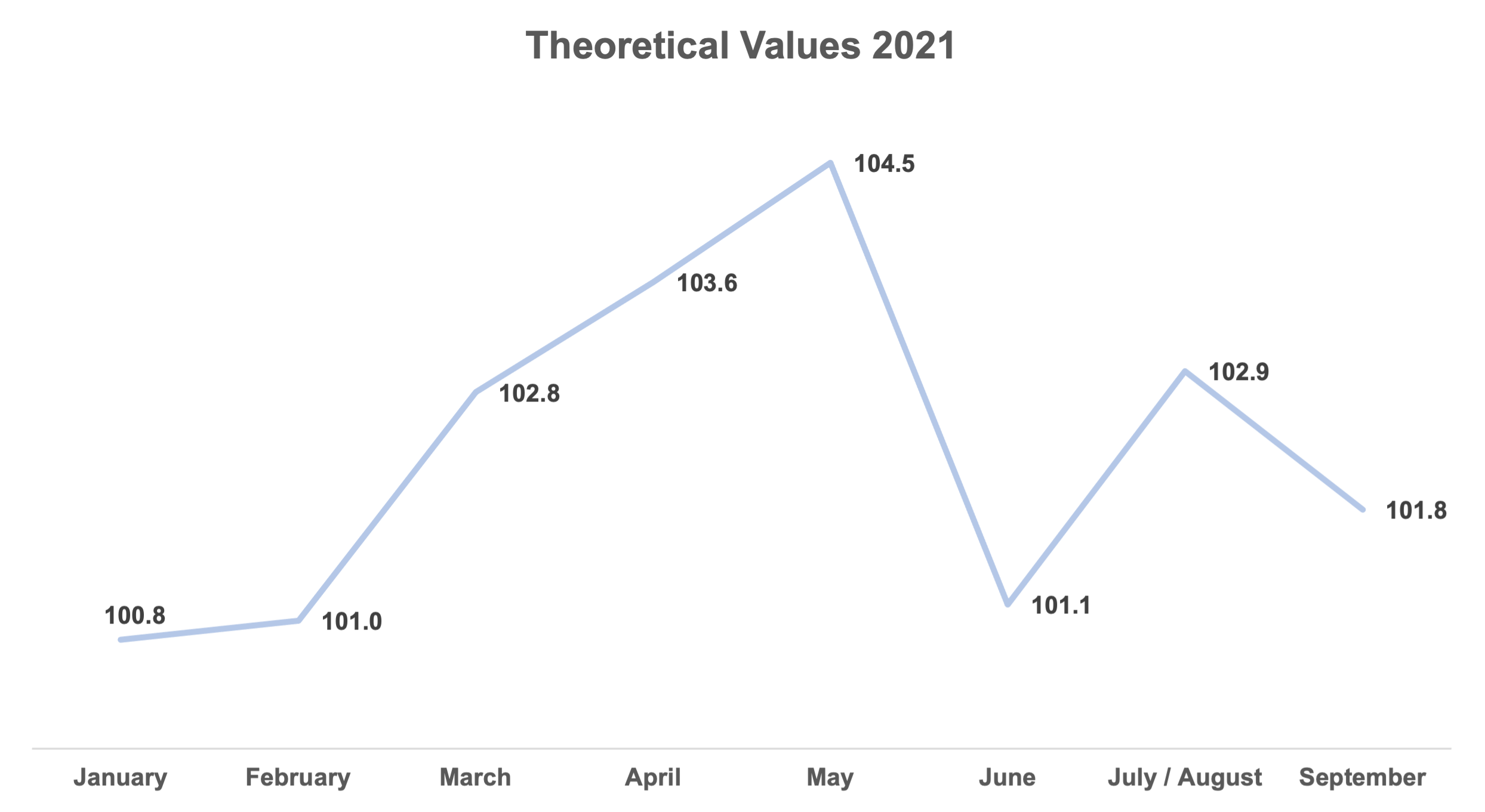

- Pricing Results: Theoretical Value. We have updated the theoretical value graph below with Q3 data (combined July and August given only one deal in July). Again, the theoretical value shows how much the typical deal was “worth” in a convertible value model based on the banks’ credit and volatility assumptions. The Q3 average of 102.3 was in-line with the 102 – 102.5% typical long run average on this metric. Additionally, it is positive to see that the surge of supply in September was met with great investor receptivity, as deals priced much tighter on a theoretical value basis.

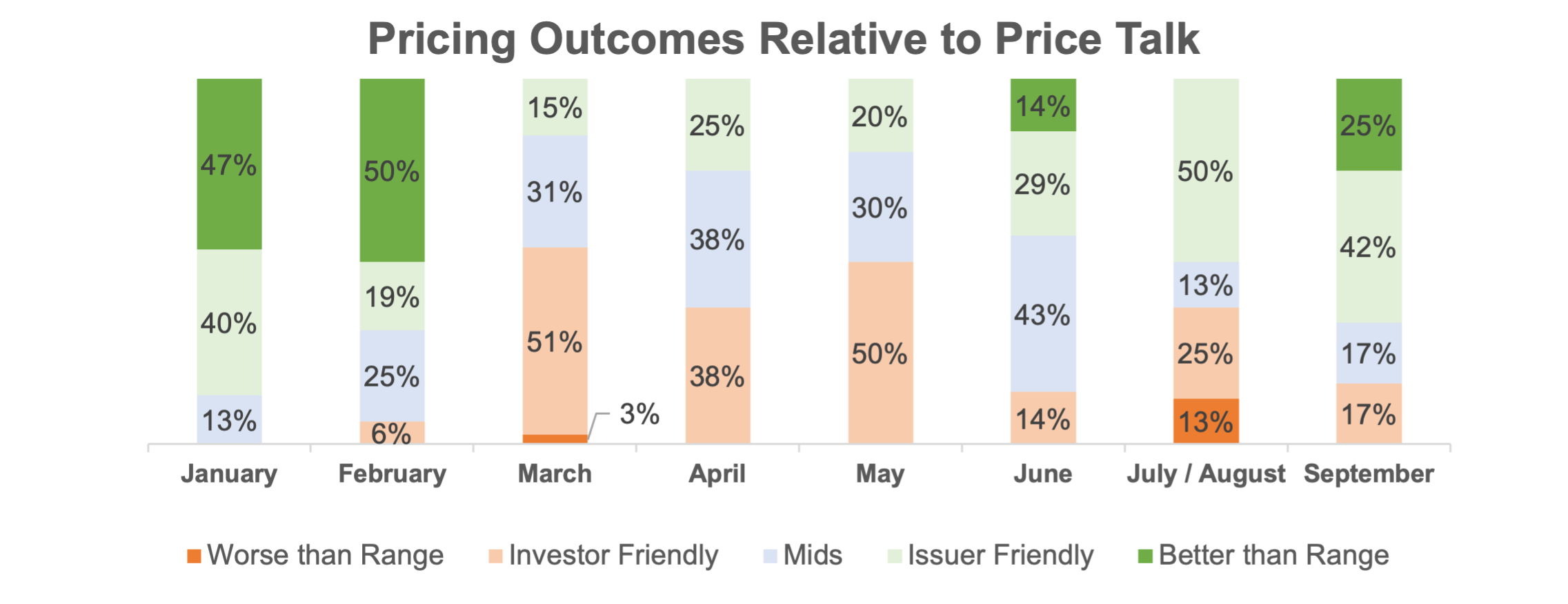

- Pricing Results vs. Price Talk. As expected, not only did deals begin pricing on a tighter theoretical basis, but also more commonly priced toward the “Issuer Friendly” side of the marketing range. The two marketed deals that priced toward the “Investor Friendly” end of the range came during the first true week of issuance in September, representing how the market strengthened throughout the month.

- Day 1 Trading. On average, for the quarter, deals traded up 2.0 points on a stock-price adjusted basis on the first day of trading (1.8 points in July / August and 2.1 points in September), compared to an average since May 2020 (post COVID) of ~1.7. This does signify that issuers left slightly more money on the table in September than they did earlier in the quarter. However, it may mean that price talk ranges set by issuers and banks “lagged” the strength of the market: investors were slightly more receptive to new issuances than the issuer side expected. Thus issuers this coming quarter may be able to tighten terms into the strength if it continues.

Related Articles