As part of our market update series, please see the summary below of what we saw in the convertible market in October and November 2020.

- New Issuance. October and November 2020 saw 5 and 12 new issue convertible deals, with dollar volumes of $2.0 billion and $8.7 billion, respectively. The 2020 year to date total stands at $98 billion in 168 deals, compared to full year totals in 2018 and 2019 of $47 billion and $57 billion.

Tech / Communications deals represented 9 of the 17 deals, with an additional 3 from the healthcare sector.

- Terms. In the table below, we compare terms to previous periods both before and after the Covid-19 pandemic. The statistics for Q4 to date were extremely attractive, with deals such as the dual-tranche Square offering pricing at 0% up 62.5% for a 5.5 year and 0.25% up 62.5% for a 7 year.

There were several other data points that the aggressiveness of the market took even underwriters by surprise. Of the 17 transactions, 10 (59%) priced better than the range from the issuer’s perspective; compared to 19 of 151 (13%) achieving this in the first 9 months of the year.In addition, while the the average model value of terms was, based on marketing credit / volatility assumptions, 102.3% of par during this period, in line with a ~102 longer-run average, several deals (Redfin, Square, Guardant Health, and NextEra Energy Partners) priced at levels modeling to less than par.

- Day 1 Trading. Deals on average traded on a stock-adjusted basis in line with their long-run average, +1.6 points, with the larger deals ($500mm+) trading up on average 1.0 point and smaller deals +2.7.

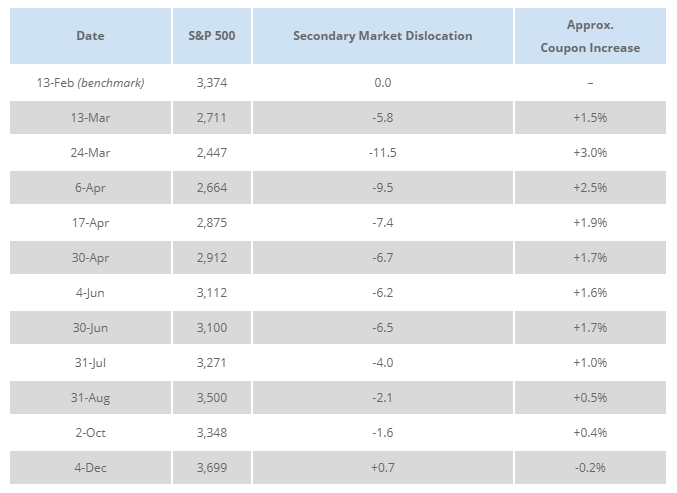

- Secondary Market. Finally, we are updating our data tracking that we launched earlier in the year tracking the dislocation in the convertible secondary trading market for a fixed universe of bonds since pre-Covid-19 in February.The market has now recovered to a point where our universe of bonds (on average) is trading at a higher implied price than pre-Covid-19. This is more confirmation that it is an attractive time to be an issuer in this market.