In the U.S. convertible market, about half of new deals are accompanied by call spreads, a transaction in which issuers purchase a derivative from banks that raises the effective conversion premium of the transaction to levels not typically available from the convertible market (e.g., 100% premium to stock price rather than the ~30% conversion premiums typical in recent quarters).

In this article, we talk about the different types of commonly used call spreads and recent market trends. In particular, we describe the decisions that convertible issuers make in choosing the type of call spread they execute. In terms of market trends, we (unsurprisingly) observe a large downward shift in the use of bond hedge plus warrant structure at the end of 2017 when the U.S. corporate tax rate was reduced from 35% to 21%. Second, we see a gradual shift towards tax-integrated capped calls over non-tax integrated capped calls in the more recent years.

Structurally, issuers employ three basic types of call spread derivatives:

- Bond hedge + warrants: The call spread is embodied in two separate documents: a purchased call option matching the conversion price of the notes, and a separate sold warrant at a higher strike price. This version is typically slightly cheaper upfront and offers the largest tax deductions — two to three times the deductions of a capped call. But there are several reasons why issuers do not choose this structure if U.S. cash taxes are not a priority. Some include possible slippage in change of control situations, more dilutive EPS computations when outstanding, and overall complexity.

- In a capped call, the call spread is combined into a single document: a purchased call option matching the conversion price of the notes, with a “cap” on the payout of the option set at the higher strike price.

- Capped calls can be designed to be tax integrated, i.e., with features that permit the capped call to be “integrated” with the convertible security and its cost deductible over the life of the security. Salient features include the options automatically exercise upon conversion and other documentation features coupling the options with the notes themselves (including a cap on the termination value in the context of a change of control).

- If any of the requirements for tax integration such as not including any of the foregoing features or the capped call is not mechanically matched up to the bond (or if the issuer does not elect to integrate) then the capped call is non-tax integrated. This allows for a bit more flexibility in handling the derivative in the event of bond repurchases, conversions or corporate actions, and is particularly a popular choice among companies who are not U.S. taxpayers.

2018 Transition Away from Bond Hedges + Warrants

When the U.S. corporate tax was cut from 35% to 21%, the convertible market saw a dramatic shift away from the use of bond hedge plus warrants and towards capped calls.

| Bond Hedge + Warrants | Capped Calls | Total | |

|---|---|---|---|

|

2017 (Pre-Tax Cut) |

70% (16) |

30% (7) |

23 |

|

2018 (Post-Tax Cut) |

33% (16) |

67% (33) |

49 |

The decrease in corporate tax rate decreased the value of the incremental deductions of the bond hedge + warrant structure compared to capped calls. Yet the non-tax costs of the bond hedge + warrant structure remained unchanged. As a result, for some fraction of issuers — such as those with a high probability of experiencing M&A or where tax deductions were uncertain due to net operating losses (NOLs) — the relative costs of the bond hedge + warrant structure exceeded the smaller tax benefits and they shifted to capped calls.

This shift has been enduring: in each year since 2018 the proportion of capped calls has exceeded 70%.

Shift in Capped Call Type

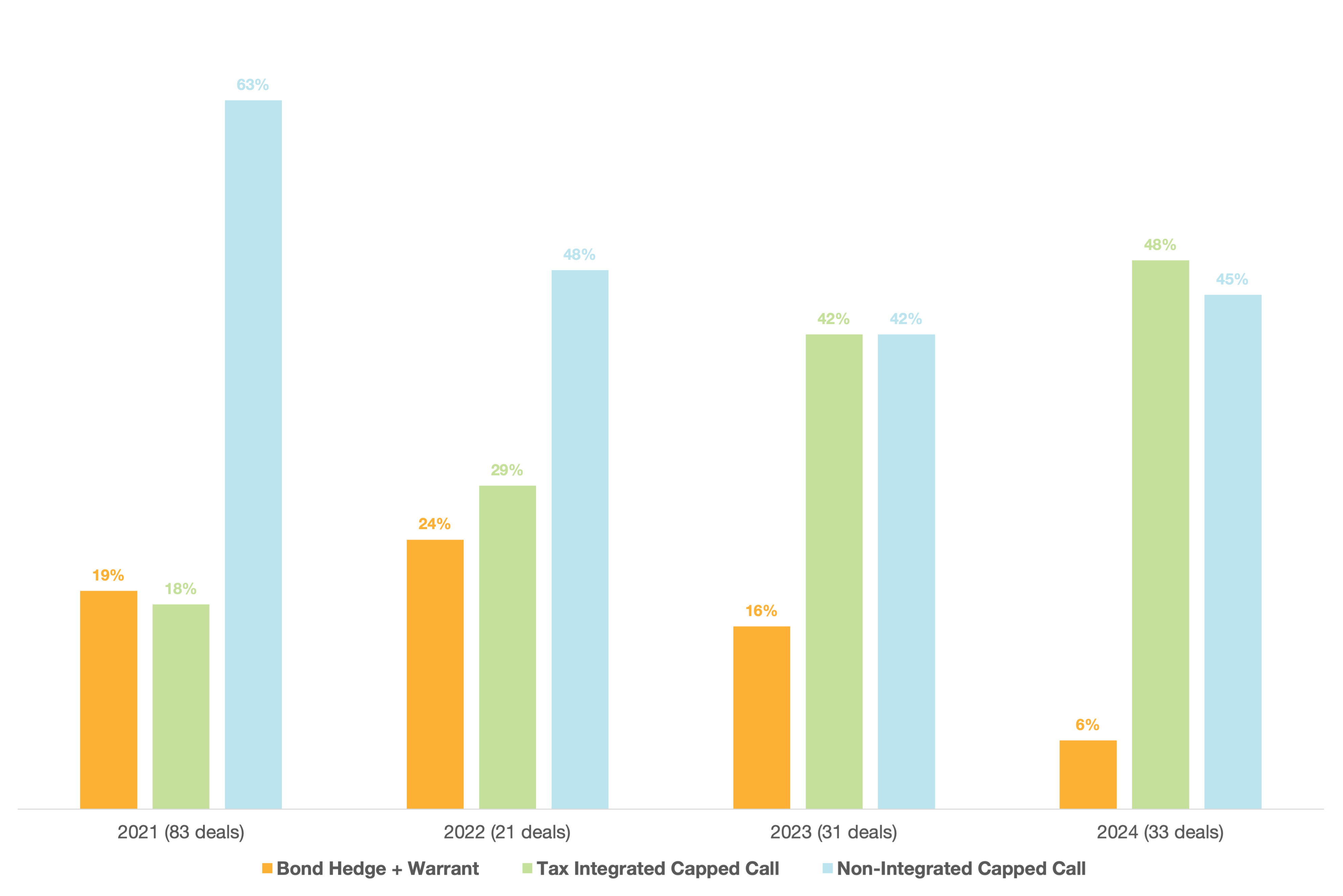

A more subtle shift has been within the capped call universe in the last several years. Using Matthews South’s software capabilities, we analyzed the capped call documents publicly filed by convertible issuers in 140 deals since 2021 for documentary indications whether the transactions were structured to be tax integrated.

There has been a large increase since 2021 in the proportion of deals being structured as tax integrated capped calls and a decrease in the proportion of non-integrated capped calls.

This may be driven by several dynamics:

- Cohort Effect. 2021 saw a wave of activity in the capital markets driven by near-zero interest rates and extremely risk-on equity market sentiment. A large number of convertible issuers were de-SPAC companies and earlier stage technology companies, many of whom had no taxable income and would not be likely taxpayers for some time. These issuers would likely value the (even if small) increased flexibility of the non-integrated structure over the near-zero value tax benefits of integration. As this market dynamic passed in more recent years, those who valued tax deductions started to represent a higher proportion of convertible issuers.

- Practice Shift. It takes time for market practitioners (e.g. banks, tax and and financial advisors, law firms) to adopt new practices. Over time, as more taxpayers shifted away from the bond hedge + warrant structure, the tax-integrated capped call documentation likely received increased focus and was modernized, and practitioners became more comfortable with the structure.

This analysis shows some of the power of our software and analysis to assist our clients in understanding trends in the capital markets. We monitor all facets of the market as they continuously develop.

Personal Views: The views expressed in this report reflect our personal views. This blog post is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. The large majority of reports by us are published at irregular intervals as appropriate in our judgment and ability to produce, so updates may not be made or available even when circumstances may have changed.

No Offer: This analysis is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. You must make an independent decision regarding investments or strategies mentioned on this website. Before acting on information on this website, you should consider whether it is suitable for your particular circumstances. You should not construe any of the material contained herein as business, financial, investment, hedging, trading, legal, regulatory, tax, or accounting advice. The price and value of investments referred to in this analysis and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. You may want to consult your attorney, and business, tax and accounting advisors concerning any contemplated transactions.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Matthews South, Inc.