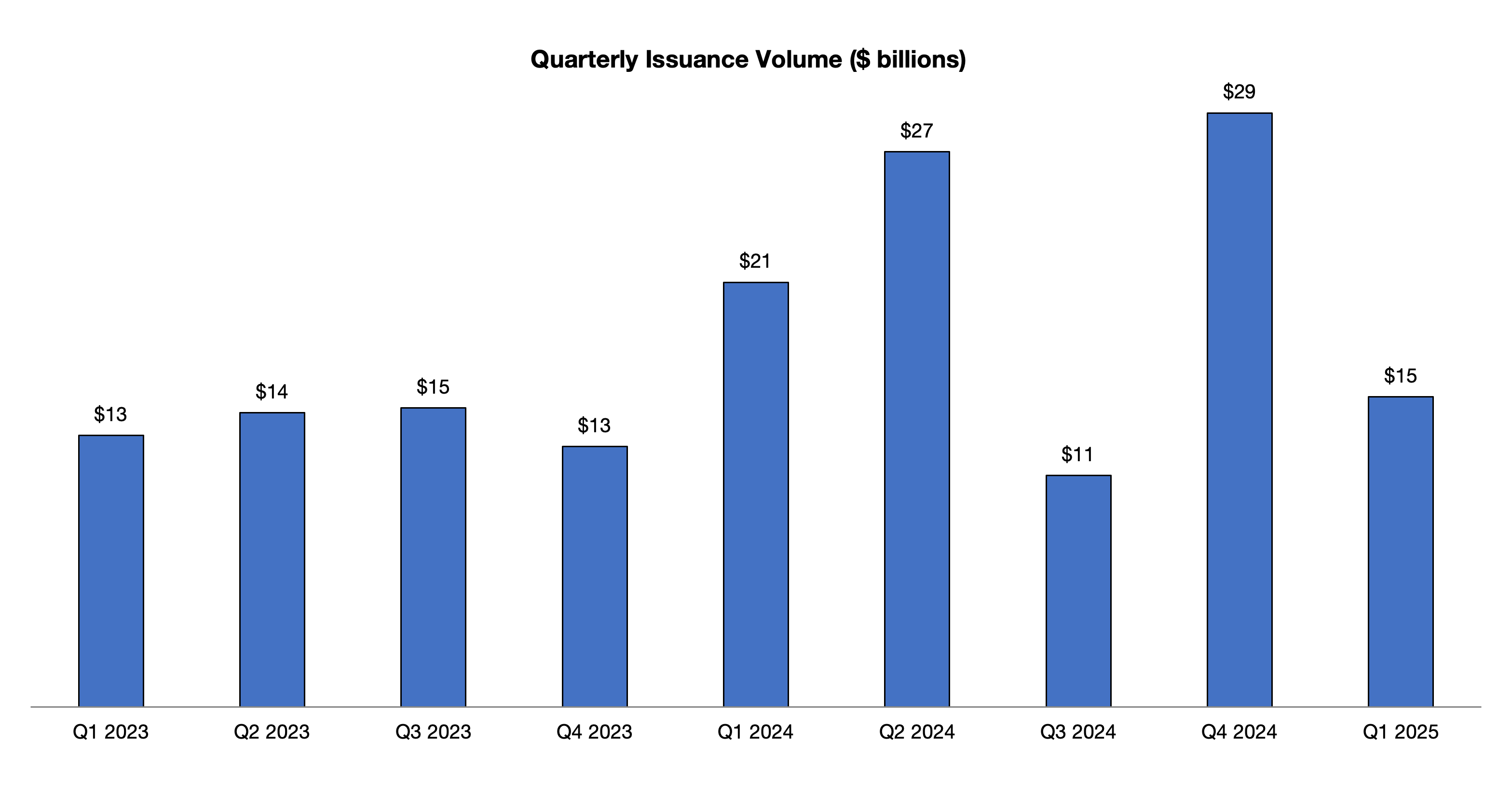

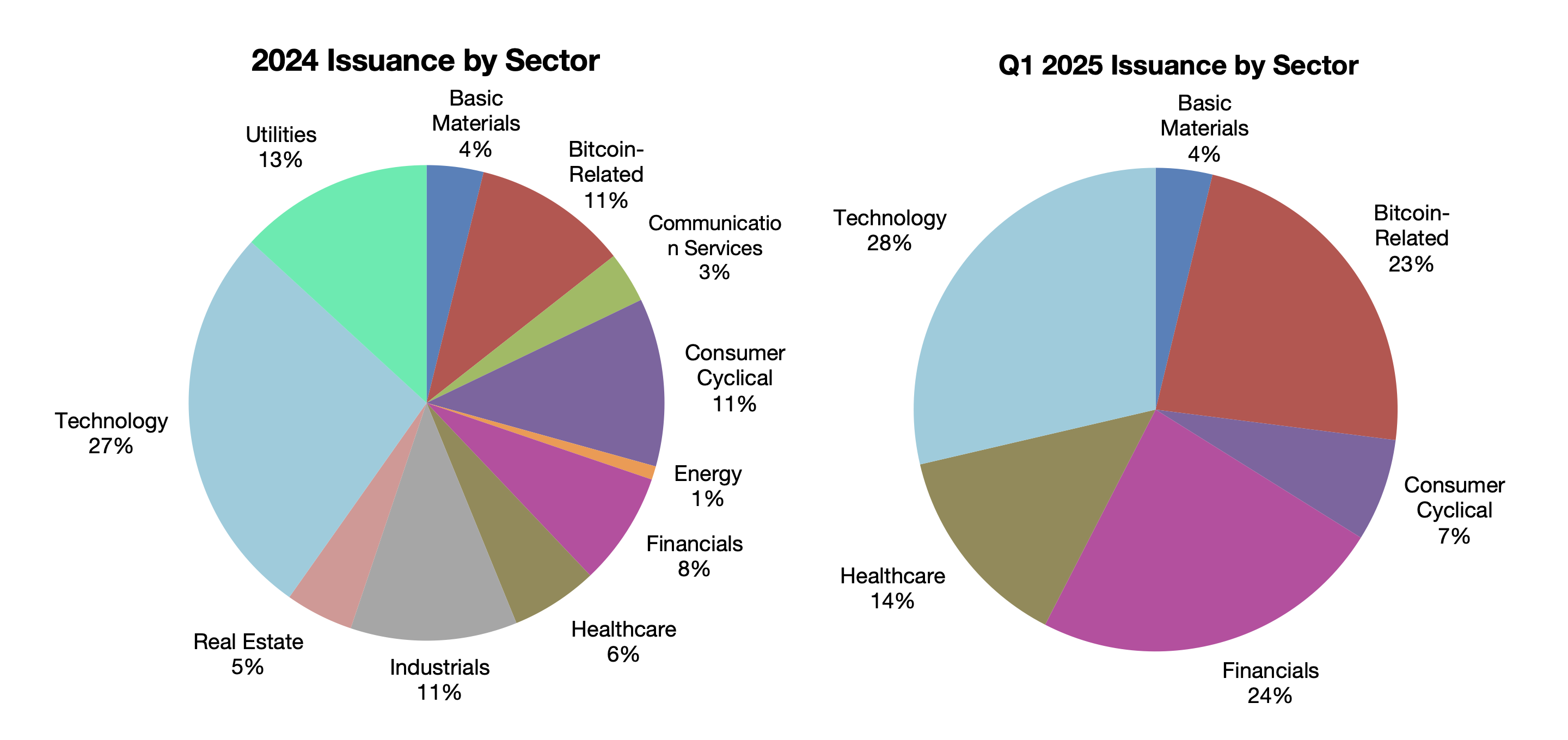

- New issue activity in Q1 totaled $15.1 billion, tracking 31% below 2024 issuance levels but in-line with historical averages. Potential issuers have remained on the sidelines to start the year given the uncertain macroeconomic backdrop.

- Refinancing activity continues to be a major theme in the convertible market, with nearly half of all issuers in Q1 using proceeds to refinance existing convertibles or straight debt.

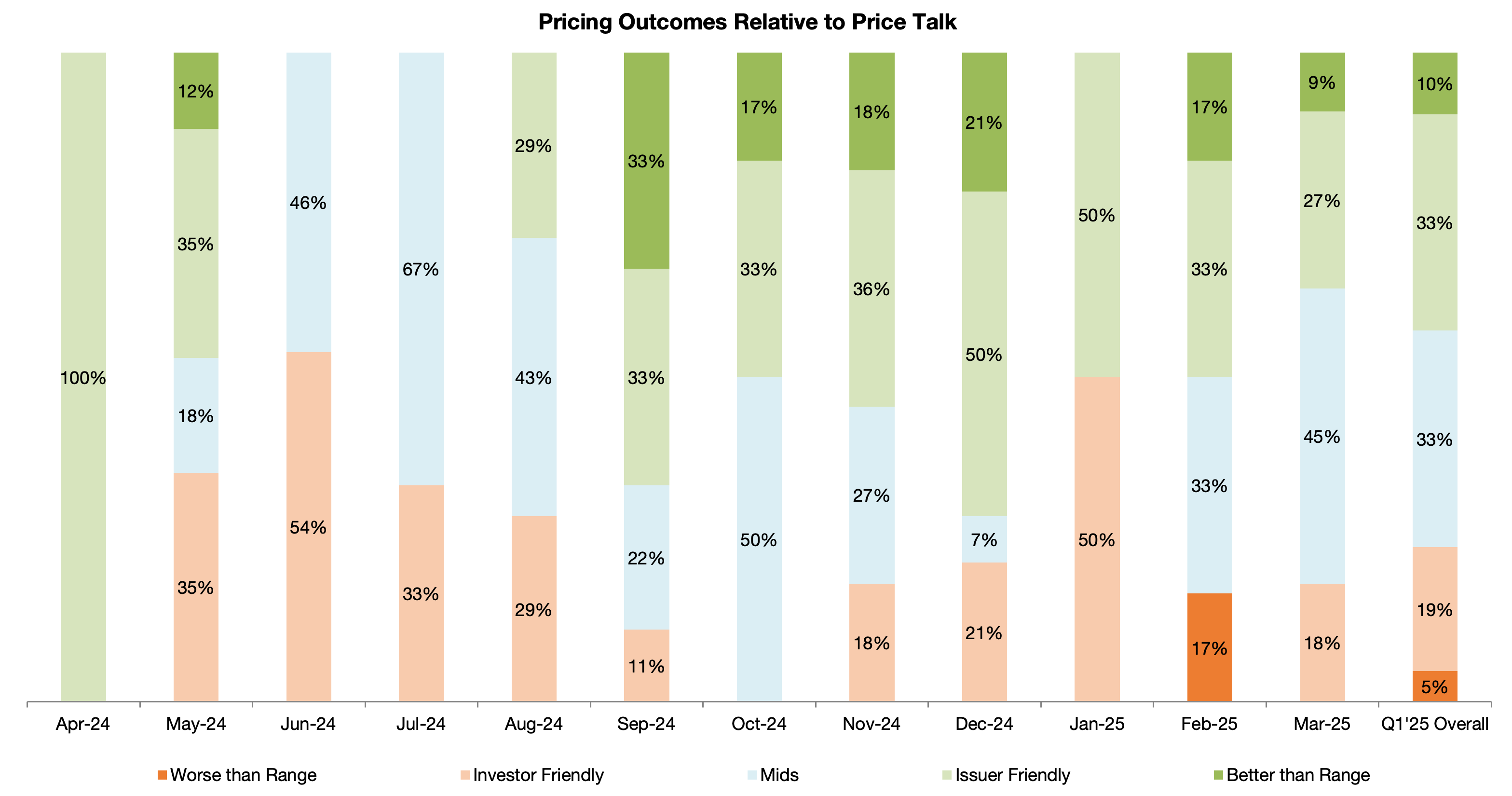

- One-third of all deals priced on an overnight basis in Q1, which is the highest proportion in the last two years. We expect issuers will continue to use the overnight execution format to minimize market risk in the current volatile environment.

- Convertible asset class remains well bid as hedged investors achieved positive returns on the quarter, despite a risk-off sentiment in broader financial markets.

Terms: The new issue environment in Q1 remained fairly constructive, as higher rates and credit spreads were slightly offset by higher volatility. The average coupon of 2.16% in Q1 is an improvement over average 2024 levels, but that is partially a function of a greater portion of the issuer base coming from technology and bitcoin-related sectors. Within the technology and healthcare sectors specifically, the average coupon widened relative to Q4 2024 levels.

Average Convertible Debt New Issue Coupon Rate and Conversion Premium 2022 – 2025

| Sector | 2022 | 2023 | 2024 | Q4 2024 | Q1 2025 |

|---|---|---|---|---|---|

|

All Deals |

3.45% / 29% |

3.50% / 30% |

2.62% / 31% |

1.88% / 33% |

2.16% / 31% |

|

Technology |

2.68% / 31% |

2.80% / 27% |

1.86% / 34% |

1.34% / 37% |

2.04% / 31% |

|

Healthcare |

3.08% / 30% |

2.56% / 30% |

2.69% / 31% |

1.75% / 33% |

2.16% / 33% |

|

Average 5y UST |

3.00% |

4.06% |

4.13% |

4.12% |

4.25% |

Personal Views: The views expressed in this report reflect our personal views. This blog post is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. The large majority of reports by us are published at irregular intervals as appropriate in our judgment and ability to produce, so updates may not be made or available even when circumstances may have changed.

No Offer: This analysis is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. You must make an independent decision regarding investments or strategies mentioned on this website. Before acting on information on this website, you should consider whether it is suitable for your particular circumstances. You should not construe any of the material contained herein as business, financial, investment, hedging, trading, legal, regulatory, tax, or accounting advice. The price and value of investments referred to in this analysis and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Matthews South, Inc.