As part of our market update series, please see the summary below of what we saw in the convertible market in Q1 2023 along with some key takeaways.

- Q1 volume of $13.2 billion was the highest in a quarter since Q4 2021

- Technology issuers regained dominance, accounting for 38% of the deal count and 44% of volume (both up from 2022)

- Rising interest rates continue to push up coupons and lower conversion premiums (~3.76% average coupon / ~30% average conversion premium); however, issuers are adapting to the new interest rate environment and tapping the market anyway

New Issuance. Q1 2023 saw 24 new issue convertible deals (all debt) with a total volume of $13.2 billion, which surpassed issuance levels for every quarter since Q4 2021. After the broad market selloff in 2022, equities rallied in Q1, with the S&P 500 and Nasdaq indices gaining 7% and 17%, respectively, giving issuers the ability to raise at higher stock prices. Average deal size in Q1 was $550 million, which is in-line with the average since 2021.

The below chart shows the breakdown of deal count and volume from each sector. Technology bounced back to a more normal share of the issuance pie after accounting for only 25% of total deals and 28% of volume in 2022. It is also worth noting that the Utilities sector, which is typically a quiet sector in the convertible market, saw three large deals this past quarter totaling $3.3 billion.

| Sector | Deal Count | Volume ($bn) |

|---|---|---|

|

Technology |

9 |

5.8 |

|

Utilities |

3 |

3.3 |

|

Consumer |

3 |

2.0 |

|

Healthcare |

3 |

1.2 |

|

Financials |

3 |

0.42 |

|

Energy, Industrials, Materials |

1 each |

0.45 total |

Terms. We can see below how convertible terms have progressively gotten weaker since 2021 in line with rates, as we are now over a year into the rate hike cycle. However, even with the wider terms, the fact that Q1 saw elevated volume compared to 2022 may signify that companies have now becoming more accepting of the higher interest rate environment.

Average New Issue Coupon Rate and Conversion Premium 2021-2023 YTD

| Sector | H1 2021 | H2 2021 | H1 2022 | H2 2022 | Q1 2023 |

|---|---|---|---|---|---|

|

All Deals Average |

0.97% / 39% |

1.20% / 37% |

2.85% / 31% |

3.52% / 28% |

3.76% / 30% |

|

Tech Sector Average |

0.31% / 44% |

0.51% / 40% |

2.02% / 33% |

2.91% / 31% |

3.14% / 30% |

|

Healthcare Sector Average |

1.36% / 35% |

2.28% / 31% |

2.44% / 33% |

3.07% / 29% |

2.33% / 29% |

|

Average 5y UST |

0.73% |

0.99% |

2.39% |

3.61% |

3.81% |

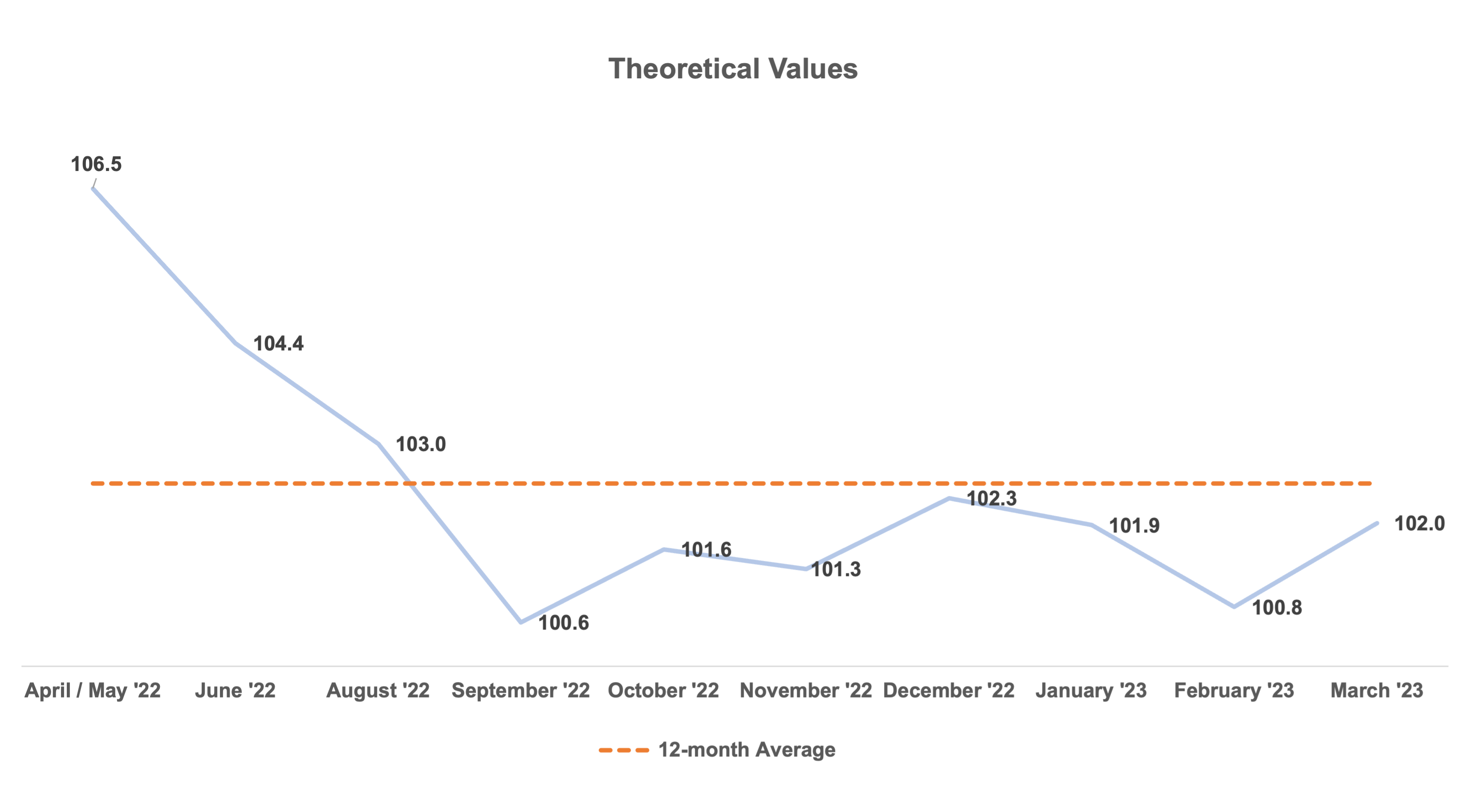

Pricing Results: Theoretical Value. The graph below shows how much cheapness deals have priced with over the past 12 months. The Q1 average was 101.3, slightly below the 12-month average of 102.5 and 3-year average of 102.8. This suggests that the convertible market has normalized relative to the broader rate / credit (whereas in mid-2022, where deals were pricing 3-6 points cheap, issuers and banks were still playing catch-up to quickly changing conditions).

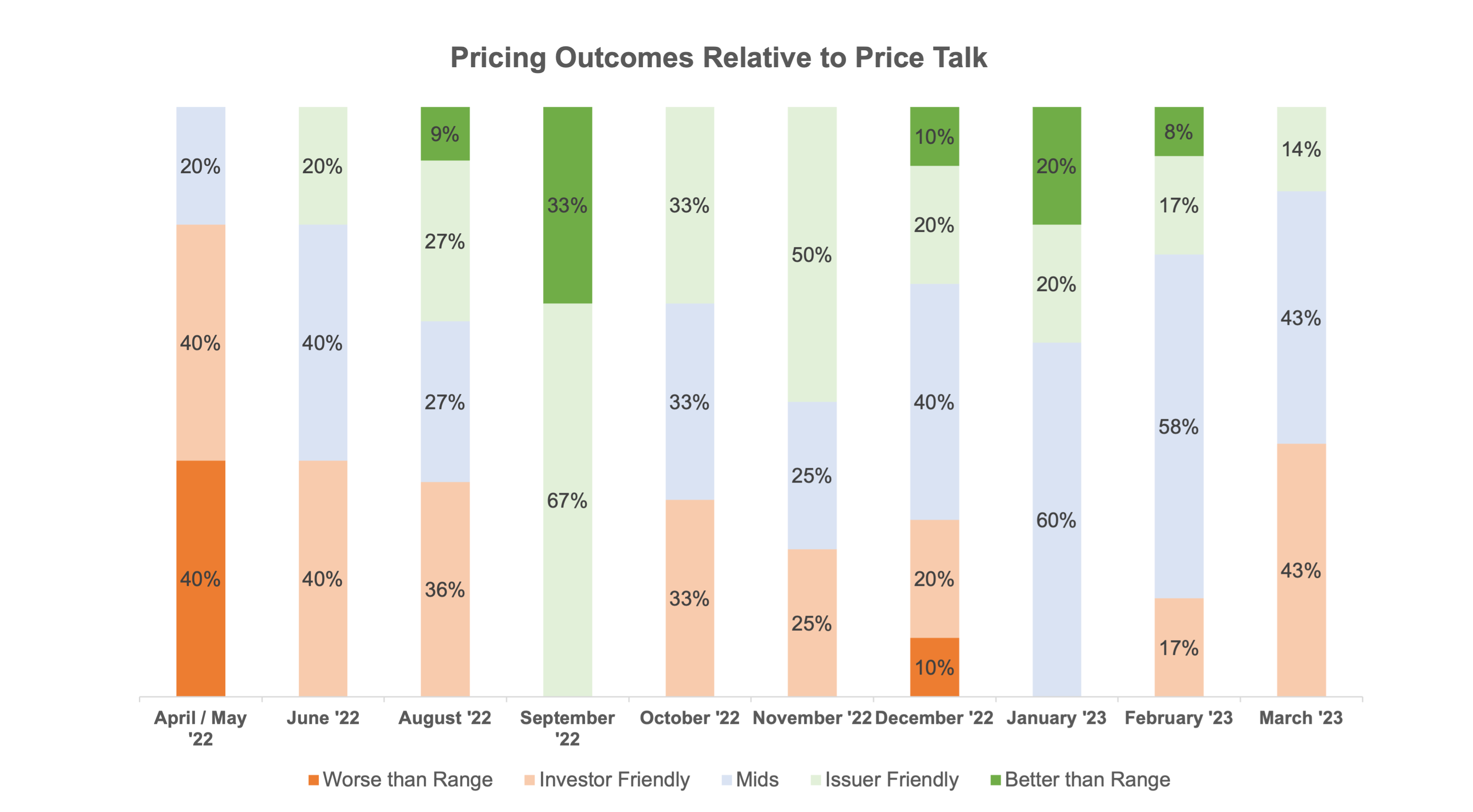

Pricing Results vs. Price Talk. Per the below, pricing outcomes were relatively balanced across the marketing range throughout Q1 with the majority of deals coming at the mid-points of the marketing ranges.

Day 1 Trading. On average for the quarter, deals traded up 1.2 points on a stock-price adjusted basis on the first day of trading compared to a 1.5 point average in 2022. The slightly less “expansion” in the secondary market is a good sign for issuers, as it indicates that not much money was “left on the table”.

Personal Views: The views expressed in this report reflect our personal views. This blog post is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. The large majority of reports by us are published at irregular intervals as appropriate in our judgment and ability to produce, so updates may not be made or available even when circumstances may have changed.

No Offer: This analysis is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. You must make an independent decision regarding investments or strategies mentioned on this website. Before acting on information on this website, you should consider whether it is suitable for your particular circumstances. You should not construe any of the material contained herein as business, financial, investment, hedging, trading, legal, regulatory, tax, or accounting advice. The price and value of investments referred to in this analysis and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.