This is the second of a three-part series of posts examining the redemption features of warrants in post-SPAC public companies. In the first post, we described typical redemption features in warrants. Here we introduce economic frameworks for how issuers can approach the decision whether and when to redeem warrants. In the final post, we will review market data on redemptions that have occurred.

Recall that SPAC warrants typically have two redemption features:

- An “intrinsic value” redemption where issuers effectively force investors to exercise their warrants for the in-the-money value. This redemption is usually available at stock prices above $18.00 per share.

- A “make-whole” redemption, under which issuers can force investors to exchange their warrants for a fractional number of shares that is formulaically determined as a function of stock price and remaining time to warrant expiry (meant to approximate the fair value of the warrant). This redemption is available at stock prices above $10.00 per share.

Make-Whole Redemption

We consider the make-whole redemption first because it is the first available method for most companies. This is because the redemption is available at stock prices above $10.00 (versus $18.00 for the intrinsic value redemption).

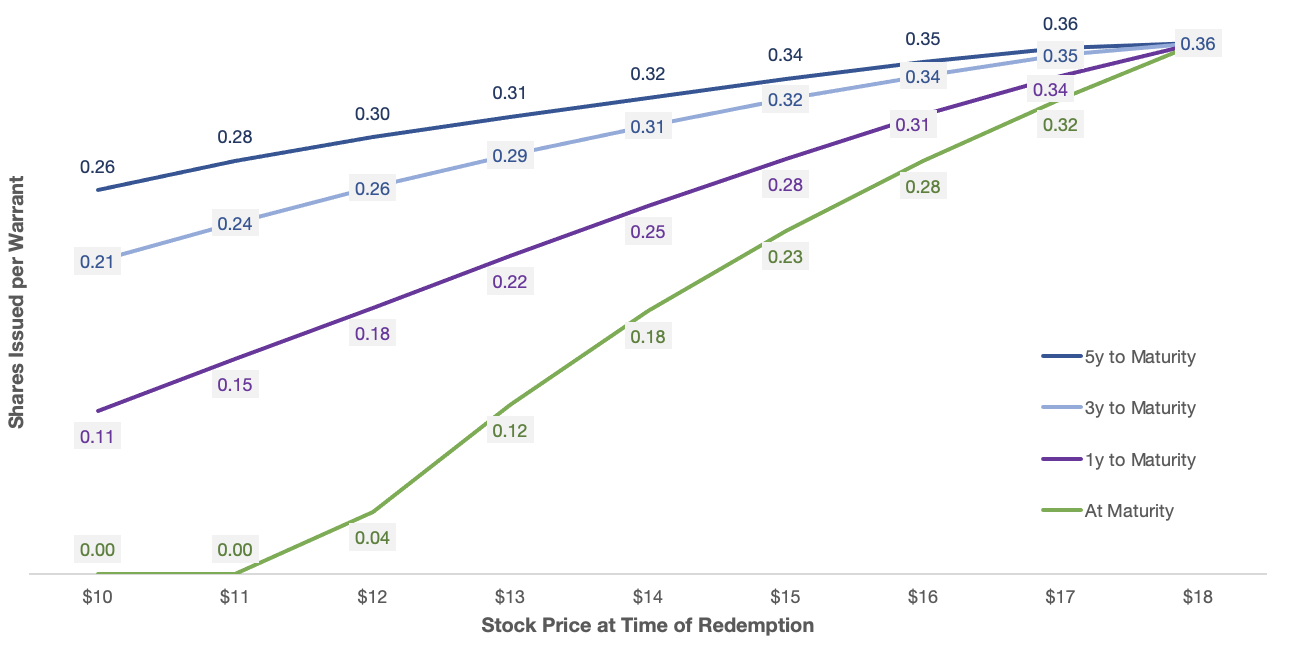

An economic analysis begins with a review of the number of shares per warrant that get issued upon redemption. The simplified chart below shows: (1) shares issued increases with stock price, as the warrants become more valuable as the underlying price increase, and (2) shares issued decreases as time passes, as the amount of time value decreases as maturity approaches until, at expiration, investors only receive the warrants’ in-the-money value (stock price in excess of $11.50 strike price).

Managing Cost of Capital of Warrants

The main reason to exercise the make-whole redemption feature is to reduce its high cost of capital in scenarios where the stock price appreciates.

For the holders, the warrants are a levered position in a company’s stock: they participate in the upside of the stock with a much smaller outlay of cash than buying the stock. If a warrant is outstanding and the stock appreciates, the cost can increase quickly for the company. For example — if the stock price is $20.00 at warrant maturity instead of $15.00 (33% higher), the warrant value at maturity is $8.50 ($20.00 minus $11.50) instead of $4.50, an 89% increase.

Above the $11.50 strike price, every incremental dollar of stock price appreciation imposes an additional $1.00 of cost (per warrant) to the company.

If instead, the warrants are exchanged for a smaller number of shares (e.g., 0.30 shares at a $12.00 stock price with 5 years remaining), the cost to the company as the stock price appreciates is more modest. At $20.00, those 0.3 shares represent a reduced cost of $6.00 (versus $8.50). Every dollar of further appreciation now only costs the company $0.30 more (versus $1.00).

However, redeeming the warrants would not be the best approach if the stock price does not appreciate post-redemption. If the stock remains at $12.00, each warrant at maturity costs the company only $0.50 ($12.00 minus $11.50). But if the company redeems now for 0.30 shares, those 0.30 shares cost the company $3.60 ($12.00 times 0.30 shares).

The reason for this is that the make-whole redemption compensates investors for time value above and beyond the then-current “in the money” value of the warrants. Thus the stock must appreciate enough to overcome this time value in order for the redemption to be break-even or better for the company.

For any given stock price and time remaining to expiry, it is possible to calculate the breakeven stock price.

| If the warrants are redeemed with 5 years left at… | Or if they are redeemed with 3 years left at…. | Then the company will issue… | Stock must exceed $___ at maturity for redemption to be cost effective: |

|---|---|---|---|

| $10.00 | $12.00 | 0.26 shares / warrant | $15.50 or higher |

| $12.00 | $13.50 | 0.30 shares / warrant | $16.50 or higher |

| $14.00 | $15.00 | 0.32 shares / warrant | $17.00 or higher |

The decision to exercise the make-whole redemption is therefore a function of the conviction the issuer has of the stock price exceeding the breakeven level. Issuers that are bullish should redeem the warrants early.

Change of Control Considerations

This economic profile – replacing the levered upside that the company owes to warrant holders with a more modest upside exposure of fractional shares – is particularly impactful in the case of a sale of the company. This is because a change of control is typically done at a significant premium to the current stock price. The acquirers bear the increased cost of settling the warrants and will reflect this breakage cost in their valuation of the company.

While disclosure / material non-public information concerns could preclude redeeming warrants shortly prior to a deal announcement, issuers in sectors likely to see consolidation may benefit from eliminating the warrant exposure sooner rather than later.

On the other side of the table, eliminating warrants prior to M&A may be helpful to potential acquisition buyers as well. Outstanding warrants may make a company’s common shares a less attractive currency for targets in a stock deal. If target shareholders are interested in participating in future upside, having a disproportionate amount of that upside go to warrant holders rather than shareholders diminishes some of that value.

Capital Structure Simplification

Finally, on a non-economic note, warrants add complexity, including mark-to-market accounting. Redeeming them (even if some dilution occurs) eliminates this overhead and can simplify the market’s understanding of the company’s valuation.

Intrinsic Redemption

By comparison to make-whole redemption, the redemption feature above $18.00 is relatively straightforward.

Economically, the company can force investors to receive the then-current intrinsic value of the warrant (stock price minus strike price). Because investors always have the right to exercise the warrants and receive intrinsic value (or can choose to leave the warrants outstanding), the redemption extinguishes all of investors’ future optionality for no incremental cost (i.e., no time value).

Translating this theoretical argument into corporate finance depends on whether the Company prefers physical settlement (issue shares and receive the strike price) or, if the warrant documentation allows it, cashless exercise (issue fractional shares equal to the in-the-money value of the warrants).

Choosing between physical settlement and cashless settlement is itself a capital structure choice. For issuers, cashless settlement means less dilution but also no cash inflow from warrant exercise. Like a stock buyback, this tends to signal confidence in the company’s balance sheet and business outlook.

Cashless Settlement

In cashless settlement, investors receive the in-the-money value of the warrants in shares at the time of redemption. As in the make-whole redemption, this replaces the levered upside exposure of 1 warrant with a less-levered upside exposure of a fraction of a share. For example, at $20.00, the computation is $8.50 ($20.00 minus $11.50), divided by $20.00, or 0.425 shares per warrant.

Because this redemption value does not include any compensation to investors for time value, the breakeven math is simple. It is cheaper to redeem than leave the warrant outstanding in any scenario where the stock price is higher at maturity than at the time of redemption.

In the $20.00 example above, if the stock went from $20.00 to $21.00, the final cost of the warrant would be $9.50 ($21.00 minus $11.50), a $1.00 increase. If the warrant had been redeemed for 0.425 shares, the final cost of those shares would be $8.925 (0.425 x $21.00), a $0.425 increase. Only if the stock finished below $20.00 would the cost of the warrant end up lower than the cost of those 0.425 shares.

Physical Settlement

Companies can view the exercise of warrants after redemption as an opportunity to raise capital equal to the number of warrants outstanding multiplied by the strike price.

While this involves selling shares below market ($11.50 vs. $18.00 or more), this is a “sunk” cost. Looking at it as a capital raise, the warrant exercise is comparable to the following two-step process: (1) sell shares in a new primary offering and (2) deliver the intrinsic value of the warrants to investors on a cash-less, net-share basis.

Step (2) of this alternative is the “cost” of seeing the warrant be exercised when the stock price exceeds the strike price. But step (1) of the alternative involves a new placement of stock, with fees to banks, lawyers, and a placement discount. Thus, the forced exercise of warrants is more efficient if the issuer is able to wait out the 30 day redemption period prior to receiving its capital and is willing to bear the risk that the stock price may fall back below $11.50, resulting in no exercise of the warrants.

Conclusion

As a general rule, redeeming the warrants under either redemption feature is an attractive proposition if the post-SPAC merger issuer expects the stock price to appreciate over the several years until the warrant maturity. How much the stock needs to appreciate is a function of how much time value must be paid as part of the redemption price. Above $18.00, no time value is paid and the stock just has to appreciate by any amount. Between $10.00 and $18.00, the redemption price is higher than the in-the-money value of the warrant, and there is a breakeven “hurdle” that the stock price must clear in order for redemption to pay off.

That said, each issuer will have its unique economic and non-economic considerations that may go into its warrant redemption decision. For detailed analysis and advice regarding your specific situation, please reach out to the Matthews South team.

Related Articles:

Post-SPAC Warrant Redemption Features (Part 1)

Post-SPAC Warrant Redemption Features (Part 3)

Pre-IPO Financing