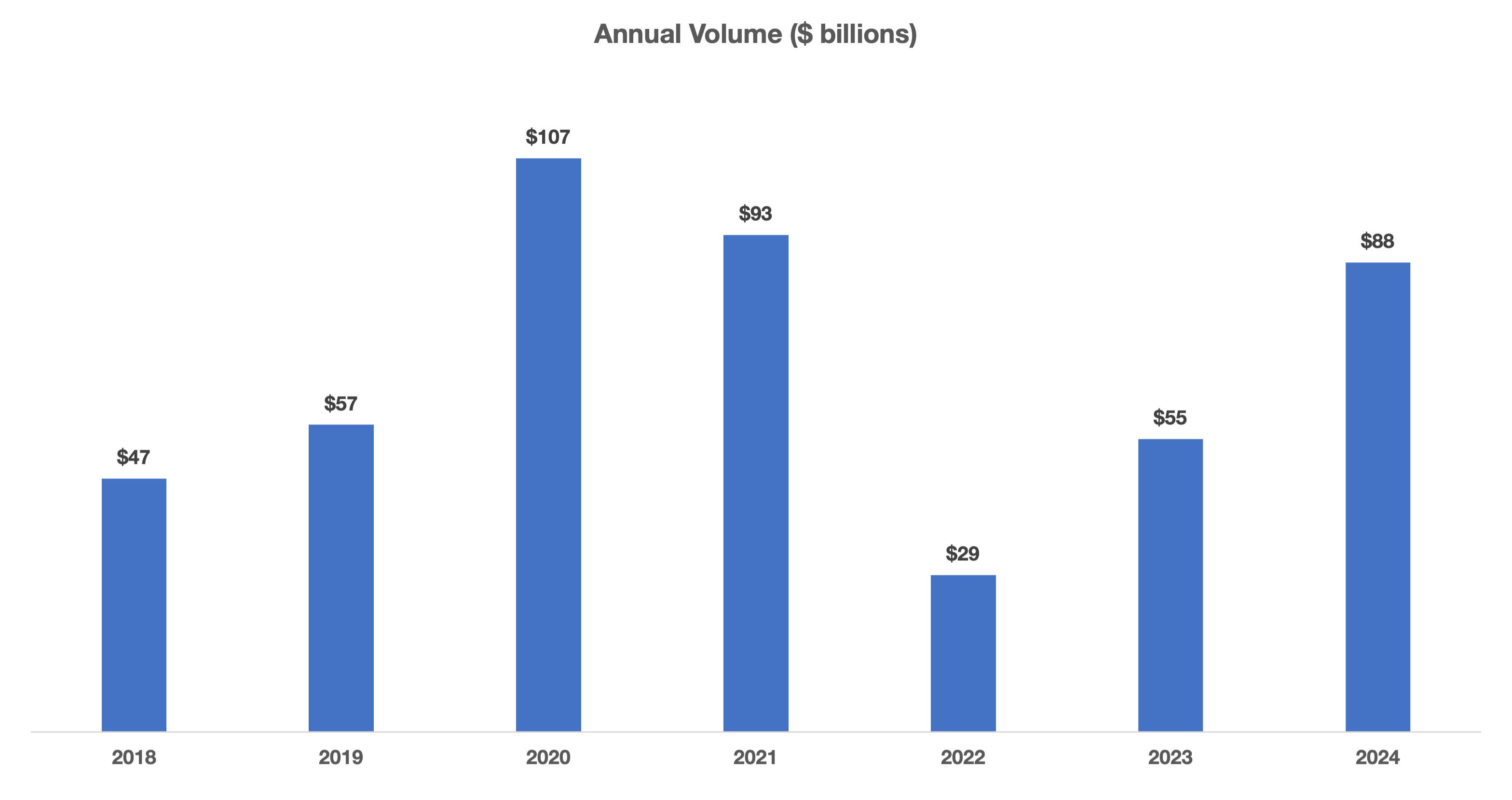

- New issue activity in the convertible market was significant with $29 billion volume in Q4, bringing total issuance for the year to $88 billion. Issuance volumes approached the pandemic-era highs of 2020 and 2021, when rates were near-zero.

- Refinancing activity has been the predominant theme among issuers in 2024. Over 60% of issuers this year raised proceeds to refinance all classes of existing debt. Convertibles offered a viable alternative to straight debt with notably lower cash interest costs in an elevated rate environment.

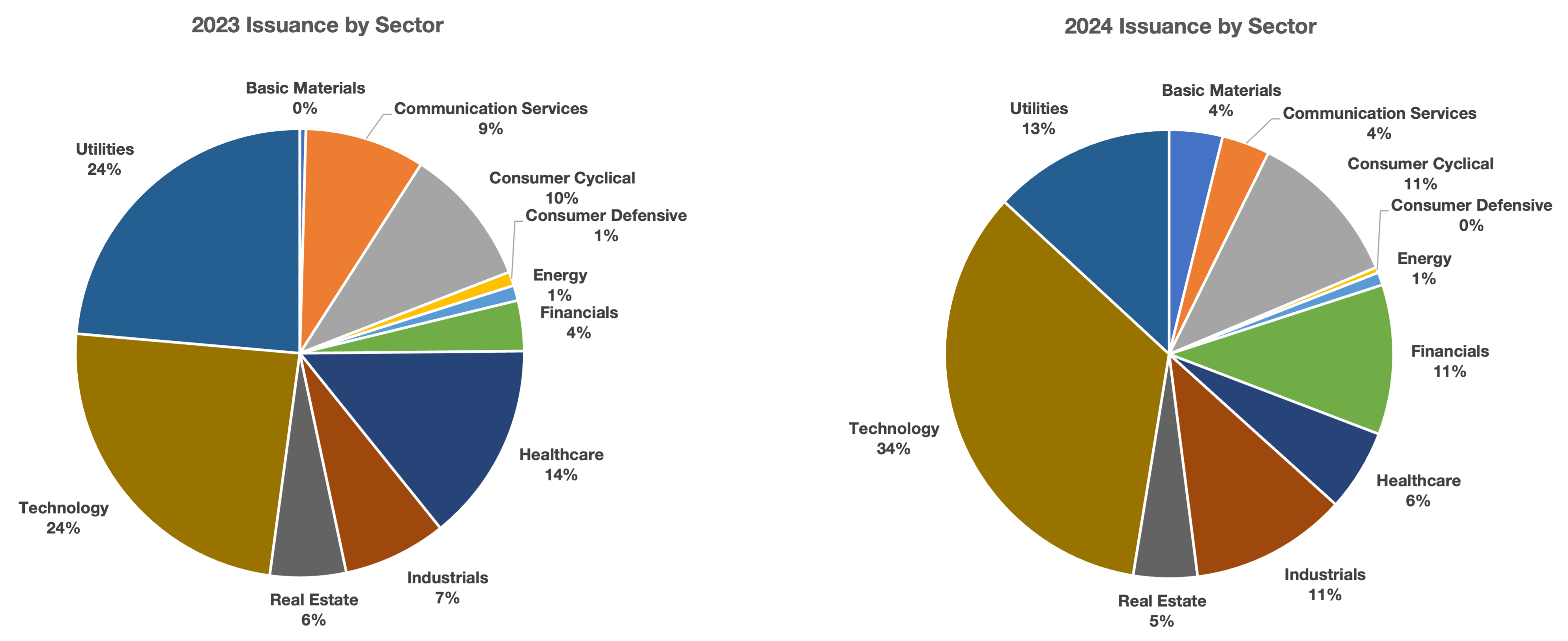

- Technology was once again the most active sector in 2024, accounting for 34% of total issuance volume. Key themes in the past year included a surge of issuance from the cryptocurrency sector as well as Chinese-domiciled issuers.

- 2024 saw the return of zero-coupon convertible debt despite persistently high benchmark rates. There were 9 deals that priced with a 0% coupon in the last four months of the year, underscoring the strength of the new issue market.

- Attractive terms coupled with all-time high share prices have made convertibles an attractive source of financing for issuers across all sectors.

The past year saw a broadening of the convertible issuer base, as tight credit spreads, elevated volatility, and attractive deal terms made the convertible market an attractive and viable asset class for a variety of issuers. Notably, there was a significant uptick in opportunistic issuance from the cryptocurrency sector and Chinese-domiciled issuers to finance share repurchases. The Technology sector led the pack once again this year, with 41 new issues raising a collective $30 billion, accounting for 34% of total volume.

Terms: The new issue environment in Q4 was extremely constructive, with the most favorable average coupon and conversion premium outcomes achieved since the market highs of 2021, despite persistently high benchmark rates. The average coupon of 1.88% in Q4 represents more than 160bps of improvement vs. 2023 levels despite marginally higher benchmark rates, which is indicative of the strength of the convertible new issue market. We saw similar patterns in the quarter for technology and healthcare companies as average coupons reached their lowest levels in the last three years. Notably, the second half of 2024 also saw a return of zero-coupon deals which were prevalent in the low-rate environment of 2021, with 9 deals pricing at a 0% coupon since September 2024.

Average Convertible Debt New Issue Coupon Rate and Conversion Premium 2021 – 2024

| Sector | 2021 | 2022 | 2023 | 2024 | Q4 2024 |

|---|---|---|---|---|---|

|

All Deals |

1.42% / 37% |

3.45% / 29% |

3.50% / 30% |

2.62% / 31% |

1.88% / 33% |

|

Technology |

0.39% / 42% |

2.68% / 31% |

2.80% / 27% |

1.86% / 34% |

1.34% / 37% |

|

Healthcare |

1.59% / 34% |

3.08% / 30% |

2.56% / 30% |

2.69% / 31% |

1.75% / 33% |

|

Average 5y UST |

0.86% |

3.00% |

4.06% |

4.13% |

4.12% |

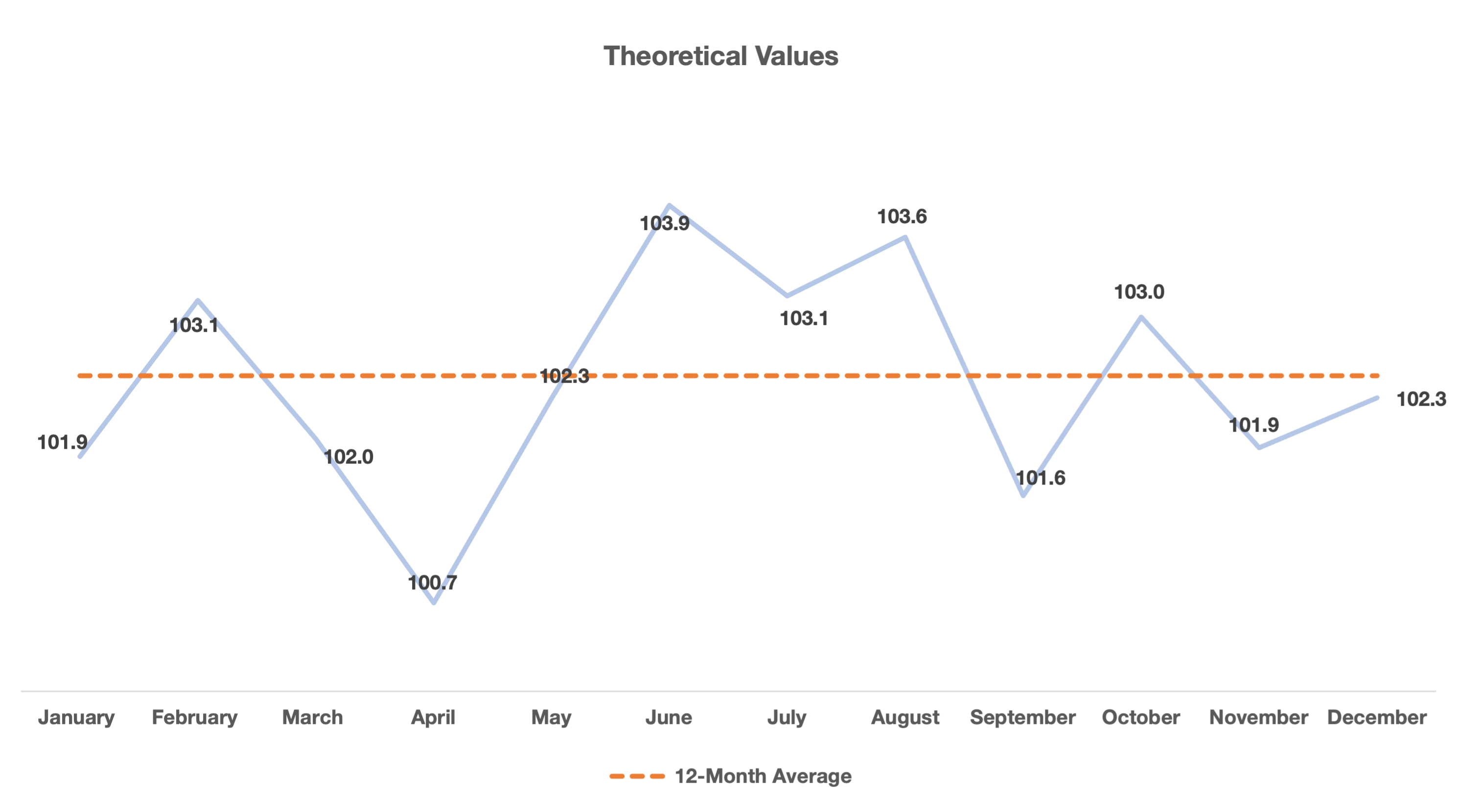

Pricing Results: Theoretical Value: The graph below illustrates the theoretical values of the deals that priced throughout 2024. A value of 100 represents a deal that priced at fair value with no “cheapness” and anything greater than 100 represents some new issue concession. The average cheapness in Q4 was 2.2 pts, below the full-year average of 2.5 pts, which represents an attractive valuation for new issue deals. With the broader market rally in Q4 and a risk-on sentiment following the U.S. election, issuers in the convertible market generally achieved attractive pricing terms at aggressive valuations due to a combination of tight credit spreads and elevated volatility levels.

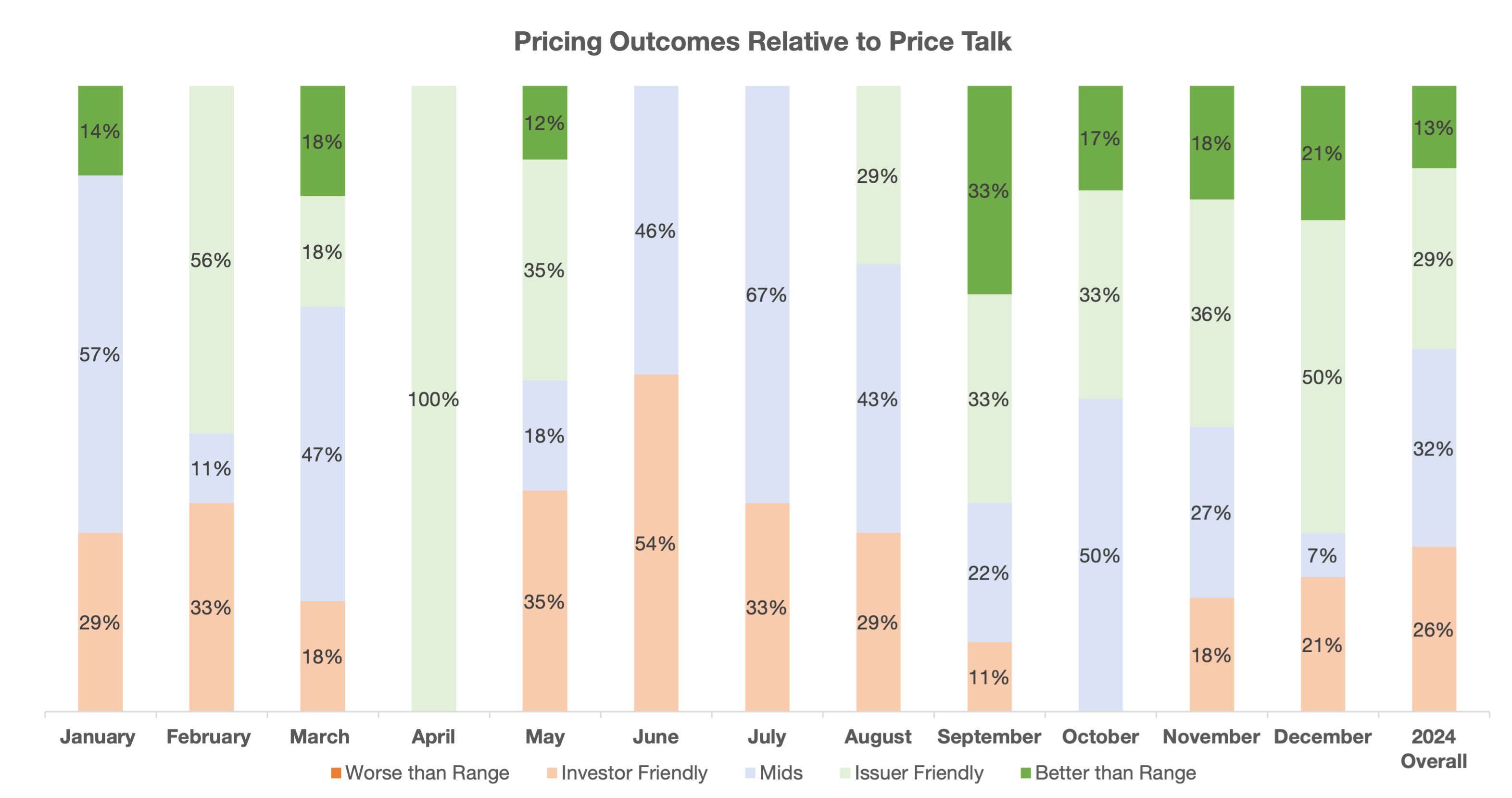

Pricing Results vs. Price Talk: As seen below, there was a noticeable trend in the last four months of the year with the majority of deals pricing better than the midpoint of the marketing range, and close to a quarter of all deals pricing better than the initial marketing range. While this trend highlights the strong demand in the convertible new issue market, it likely also indicates that there was room for banks and issuers to be more aggressive with the marketed coupon and premium ranges. The results for 2024 as a whole were more balanced, with price talk more in-line with final pricing outcomes.

Secondary Trading: Both outright and hedged investors enjoyed favorable returns in the convertible secondary market in 2024, with near double-digit returns for outright funds, while convertible arbitrage funds also achieved positive returns on the year. The start of the rate cut cycle, as well as the anticipation of pro-business policies from the incoming political administration were the main drivers of outright returns in the convertible asset class.

Personal Views: The views expressed in this report reflect our personal views. This blog post is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. The large majority of reports by us are published at irregular intervals as appropriate in our judgment and ability to produce, so updates may not be made or available even when circumstances may have changed.

No Offer: This analysis is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. You must make an independent decision regarding investments or strategies mentioned on this website. Before acting on information on this website, you should consider whether it is suitable for your particular circumstances. You should not construe any of the material contained herein as business, financial, investment, hedging, trading, legal, regulatory, tax, or accounting advice. The price and value of investments referred to in this analysis and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Matthews South, Inc.